A Tax On The Brain

Salty or tough characters like to quote the adage: “There are only two things certain in life: death and taxes.” Notice that these two inevitable things are distinctly unpleasant, but also — from a certain point of view — completely necessary.

Leaving death aside, let’s talk about taxes because, well, it’s tax season, and I’ve got to do mine. I have to do it, because that’s the law. I also kinda want to do so I can get back my refund. But neither of these motivations get anywhere near the reality at the heart of taxes: namely that governments collect taxes for our benefit: for the common good of society. If that’s true, why do most of have the unpleasant feeling of an unwelcome hand in our pocket when it comes to the topic when we’re really making a meaningful contribution into each other’s lives. (Well, we could feel Greek about it.)

There are some pretty smart people who are trying to figure that out. Notable among them is Keith Kirchler who is applying economic psychology to the field with his slippery slope framework:

You can watch to a more in-depth interview of his work if you want to get into the details of his research.

The interesting thing about Kirchler’s work is that he’s connecting the way we feel about taxes with the structure of the economy and society in a way that can be test both qualitatively and quantitatively. In sort, the actual numbers of people’s tax behavior (maybe what they actually pay relative to what they should pay) can be linked to the feeling of trust they have in the system, which is dependent on the type of power the government uses to get people to pay.

This type of research can lead to some surprising insights. For example, Alex Rees-Jones found that how you frame incentives for people can really determine how much they are motivated to comply. In Taxpayers Hate to Lose: How Psychology Can Help Increase Collection (listen to the podcast version), Rees-Jones reveals that taxpayers are more likely to comply with tax policy when you frame a certain dollar benefit as reducing a loss rather than a gain. To say that another way, people are more motivated to by the idea of not loosing $5 than they are by earning $5. Either way they get $5, but not loosing seems somehow more urgent. Rees-Jones advocates that leaders can control people’s tax behaviors simply by talking about gains when they want fewer people to act and talking about loss-prevention when they want more to do so.

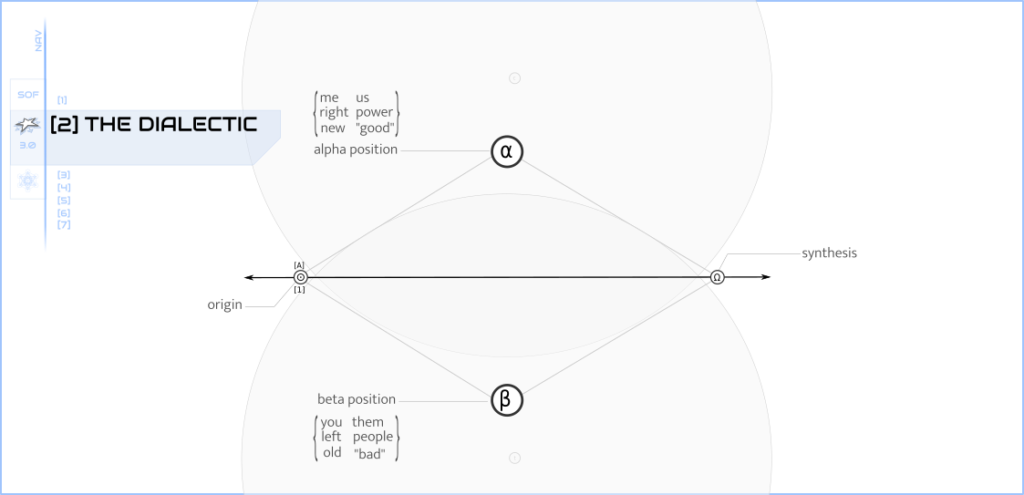

Let’s think about this in terms of the dialectic, which we’ve been using lately to think about relationships, especially between identity groups.

In a system of taxation, the two parties are taxpayers and the government — at various levels. When it comes to people, who is alpha and who is beta is purely a matter of perspective. So it shouldn’t be surprising for taxpayers to see themselves as the alpha while the reverse would be true of the government.

Whoever you see on top, taxpayers and the government generally have a competitive relationship in taxation where the government — in the form of various tax agencies — is trying to collect the maximum revenue the law allows to fund its programming while the taxpayers are trying to pay the minimum in tax.

The synthesis would come from the tax agencies and government using a fair and transparent process of assessment and collection and the taxpayers voluntarily complying with the awareness they were benefiting the good of all.

Needless to say, that’s not the prevailing emotional current one will pick up around April 14th, when federal tax filings are due. Because this costs the government money — and that has an impact on social programs — authorities have an interest in improving this reality.

When we think of [2] The Divide system shape, upon which [2] The Dialectic is based, we’re trying to work the system to produce balance through synthesis. In other words, you unify the alpha and beta not through destructive competition, but constructive collaboration. You get the two opposing forces to use their creative tension to create something new neither side could achieve on their own.

When thinking about balance through synthesis in competitive relationships like taxation, the only way to develop synthesis is to find a significant win-win. Competitive relationships seem, by nature, to focus on win-loose outcomes, but they can often actually lead to loose-loose scenarios.

When Rees-Jones talks about different tax authorities incentivizing taxpayer compliance (which means following the rules), he’s talking about creating a win-win. When people feel like they are winning in some way by following the law, they pay their taxes, which means the government is winning because they have the money they need to do things like build roads, educate children, and keep people safe.

Rees-Jones research captures an important nuance about incentives from prospect theory, a set of ideas about motivation in economics. Prospect theory discovered that, when evaluating a reward of equal value, people are more motivated to prevent a loss than to forfeit a gain. His talk is about how you can use this fact to hack human behavior to get the results you want.

That made me think of something I learned from my conflict resolution training in alternate dispute resolution. When two parties are in conflict (a type of competition), they won’t be strongly motivated to resolve their dispute if they think they will win a reward OR if they think they’ll come out even. A good mediator would spend time exploring with a dispute party their b.a.t.n.a.: “best alternative to negotiated agreement.” This mean exploring with the parties how much they will loose, even if the process of fighting or going to court turn out in their favor. When they see conflict resolution as a way to minimize their loss, they are more motivated to try to work things out.

Responses